Buying a house is one of the biggest investments you’ll probably make over the course of your life. For a lot of people, it is the largest purchase they’ll ever make. While owning your own home can be incredibly satisfying, before you dive in, it is good to be prepared so you can buy your home with peace of mind.

Preparation cannot be overestimated. As the housing crisis approached, many homebuyers were unprepared for changes in income and managing risk, often leading to foreclosure. Prior to the housing crisis, U.S. housing finance policy, for example, succeeded in building stability and prosperity for almost 70 years based on a combination of government support and regulation to stimulate the flow of private capital to affordable and lower-risk mortgage products. In the 2000s, there were mortgage products introduced into the market that were not beneficial to the consumer.

Therefore, it is vital that as you embark on the journey of buying your first home, you have sufficient incoming cash (earnings and other) as well as enough savings put aside. Before entering the world of home ownership, make sure you have been through the necessary steps required.

Therefore, it is vital that as you embark on the journey of buying your first home, you have sufficient incoming cash (earnings and other) as well as enough savings put aside. Before entering the world of home ownership, make sure you have been through the necessary steps required.

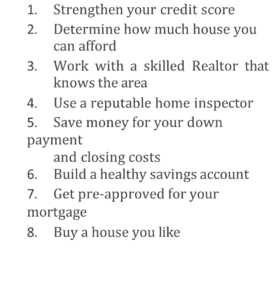

Here are some few things you need to do when purchasing a house:

STRENGTHEN YOUR CREDIT SCORE

Your credit score impacts your ability to get a loan for your mortgage payments. The higher your credit score, the lower your monthly payments will be. At 660 to 680, you are eligible for mortgage lending from most lenders. Below that score range, you will end up paying large fees or lenders will require a higher down payment.

Lenders may offer loans to borrowers who are prepared to put down larger payments if their credit scores are lower than optimal rates or the market standard (640-660), but still within the 580s. It is better if you can raise your credit score before you apply for your home mortgage. Any score above that range helps lower your interest rate and saves you significant amount over the long run.

You’ll end up with a good deal with scores of 700-720. Scores of 750 and up will pretty much get the very best rates available. Knowing this, go in prepared. Increase your possibilities of getting that mortgage loan approved for the house you want with an affordable interest rate and monthly payment by increasing your credit score. Get started by pulling up your credit report and checking for any errors. Be sure to have a consistent payment history.

In addition, wait for a whole year or longer from the time you last applied for new credit before you apply to get a mortgage loan. Wait again to apply for new credit until you have secured your home and moved in.

DETERMINE HOW MUCH HOUSE YOU TRULY CAN AFFORD

This is very important. Too often homebuyers purchase homes beyond their financial reach, then find themselves stretched and unable to make their monthly payments. Avoid this catastrophe and any associated stress by purchasing a house that falls within your affordable budget. Remember this simple rule: the monthly cost of paying for your home and all related expenses should be 28-30% of your budget or less. Anything over this amount is too expensive on a monthly basis. Knowing this, you can effectively plan out your budget. Use financial calculators to help you figure out how much you will pay for the house you want. Put aside enough money and build a nice nest egg before you buy.

WORK WITH A SKILLED REALTOR THAT KNOWS THE AREA

Every neighbourhood has its unique qualities that you want to be aware of before you buy. An agent that is well-informed about the area will also know what homes there are and their worth, which will help you avoid overpaying for a property. You want a real estate agent who knows their stuff locally!

Make sure you interview several different buyers’ real estate agents. Choose someone that is full time working in the business every day and has a recent history of successful sales. The better the real estate agent knows the area, the better equipped they will be in understanding the differences in market value from one property to the next.

USE A REPUTABLE HOME INSPECTOR.

Find a home inspector that is registered or certified, or someone your real estate agent knows and trusts. You need someone who knows what he or she is doing and is not motivated to miss issues to encourage a sale. It is also advisable to find your inspector yourself if you do not know your real estate agent well. The last thing you need is a real estate agent recommending you use their favourite inspector because he [real agent] is not that thorough. While most real estate agents are honest people, there are always a few bad apples in any industry so you need to be on the lookout.

SAVE FOR YOUR DOWN PAYMENT AND CLOSING COSTS

The next step is to put enough cash aside for your down payment. This amount can range between 3% and 20% of the home’s price.

Remember to factor in closing costs and loan fees. Closing costs can add up. Be sure to plan for these additional fees. For example, if you sign up for a $200,000 mortgage, your closing costs are typically $2,300-$4,000.

Put aside as much money as you can for your down payment and closing costs.

See Also

BUILD A HEALTHY SAVINGS ACCOUNT

You have to have a savings account in place before you buy your home, especially when you are borrowing money from a lender. One of the most important aspects lenders want to see before they approve a mortgage loan is you have genuine savings and are not dependent upon your paycheck every month. Aim to have at least three to five months of savings put aside. This money will also be helpful if you have unexpected expenses, like a new water heater or roof, which can quickly add up.

Just paying your mortgage is not the only cost you incur when you buy a house. You also have additional costs such as maintenance and repairs. This typically costs 2.5% to 3% of the cost of your home every year. Some older homes may require more repairs. If you are doing a renovation or addition to your home, you will incur more expenses. Therefore, at the very minimum, plan on putting aside cash for these maintenance and repair costs.

GET PRE-APPROVED FOR A MORTGAGE

Get pre-approved so when you are ready to buy, you have already done a lot of the heavy lifting and you will be prepared to buy a home you like. The pre-approval process is more extensive than it was a few years ago. Your documentation around income and assets is essential. This step is advisable to help you in determining to a close approximation of how much house you can afford to buy. It also reduces your stress level since you are more prepared before you meet with the mortgage lender.

BUY A HOUSE YOU LIKE

Finally, buy a house that you like and can live in for the next few years at least. Short-term ownership can be expensive and difficult because selling homes can take time. Step back and make sure you and your family really like the house before you buy.